How Virginia’s fiscal system redistributes in all the wrong ways

American political debates about taxes and public services are often framed as a choice between two competing visions. One emphasizes progressive taxation and redistribution, with the goal of ensuring that those with greater means contribute more to support shared public services. The other emphasizes limited government, lower taxes, and local responsibility, with the expectation that communities should largely fund their own priorities.

In Virginia, like many other states, we have a fiscal system that does not produce fiscal outcomes that coincide with traditional notions of fairness—regardless whether one prefers a more or less progressive fiscal system. Instead, the way we finance public services—especially public education—produces fiscal outcomes that depend less a household’s income level and more on geography. As a result, households with similar earnings can face very different fiscal burdens depending on where they live, while communities with very different needs are treated in ways that are difficult to justify on either equity or efficiency grounds.

When geography overrides fairness

To understand how this happens, it helps to consider a simple example.

Imagine four localities, each with 100 households and 100 students, each needing to spend $10,000 per student on education. Let’s call these four localities Northern, Central, Eastern, and Southern. In each of these four localities, total education spending ought to be $1 million based on the state education norm. Up to this point, there is no difference.

The divergence arises in how much of this cost must be financed locally. In a ‘typical’ locality, the state may require that 50 percent of education spending be raised from local sources, meaning the locality must generate $500,000 on its own. In wealthier localities, the state may require that 80 percent of education spending be raised from local sources (i.e., the locality must generate $800,000). In a less affluent locality, the required local contribution might be only 20 percent, or $200,000. This allocation of transfer resources reflects the state’s effort—at least in principle—to equalize across jurisdictions with different fiscal capacities.

A first potential concern—depending on one’s redistributive preferences—is that relying on property taxation to fund public education instead of income taxations shifts from the fiscal incidence from a more progressive tax to a less progressive tax.

Perhaps more significantly, regardless of redistributive preference, the problem with this approach is that not every household in a ‘wealthy’ locality is wealthy, while not everyone in a poor locality is poor. And in contrast to a state income tax—where households are taxed in accordance with their income levels regardless where they live—requiring different localities to contribute different shares will result in diverging local property tax rates, which in turn cause taxes to increase of decrease in different localities for rich and poor households alike. As the example will show, this will result in taxpayers paying a lot more or less not based on their income level (i.e., more or less progressive), but rather, simply based on the locality where they live.

A system that rewards place, not ability to pay

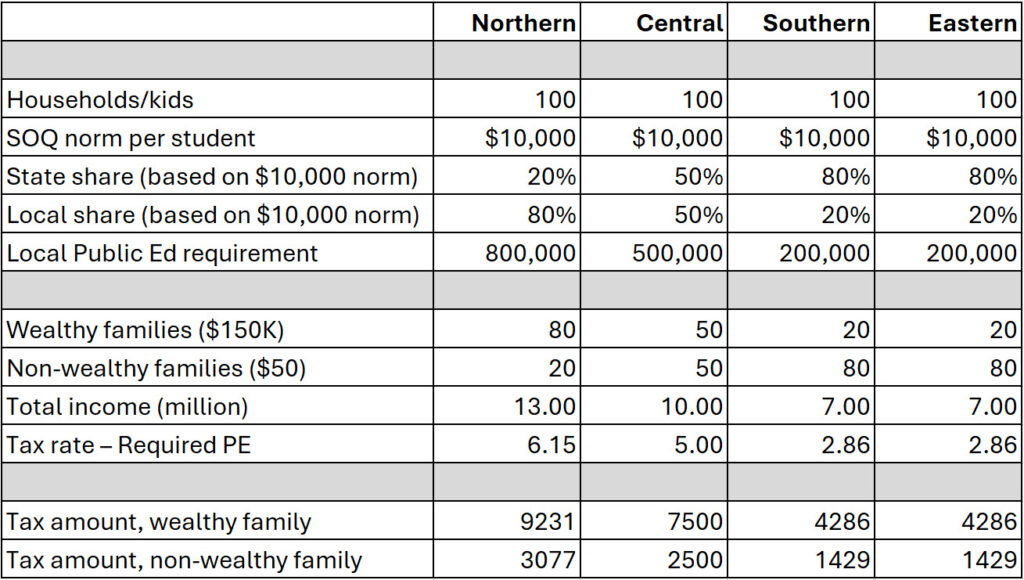

Based on the numeric example above, suppose that in the wealthier locality—Northern—there are 80 households earning $150,000 and 20 households earning $50,000. Let’s further assume that in the less affluent localities (Eastern and Southern), there are only 20 higher-income households and 80 lower-income households. Central has 50 households in each category.

As a simplifying assumption, let us assume households own homes—and pay property taxes–in proportion to their income (in other words, in each locality, a family that has an income three times higher than another family has a house that costs three times more). For the moment, we are also going to ignore other issues, for instance, differences in the cost-of-living, that cause urban income levels to be overstated and tends to make public education in urban areas more expensive.

Once the required local contribution to public education is distributed across all households in each locality, the implications of the current fiscal system become clear. In the wealthier locality, in order to collect the required $800,000 contribution to local public education, each higher-income household ends up contributing roughly $9,300 toward education, while lower-income households in the same localities are expected to contribute roughly $3,100. In the less affluent localities, the corresponding figures are significantly lower: roughly $4,200 for higher-income households and about $1,400 for lower-income households.

Numeric Example 1 (click toggle to view)

See Excel version (with formulas)

Within each locality, the fiscal system may appear “fair” (or broadly proportional) in its contributions. But across localities, the comparison is striking. A higher-income household in a poorer locality contributes substantially less than a similar household in a wealthier locality. At the same time, lower-income households in wealthier jurisdictions are expected to contribute considerably more than lower-income households elsewhere.

In fact, it should be noted that in this example, taxpayers of the same income level are paying vastly different amounts in different localities for exactly the same level of public services.

This is not redistribution from rich to poor in any consistent sense. Instead, it is redistribution based on place. Where you live ends up mattering as much as—if not more than—how much you earn.

Regional cost differences result in further divergence

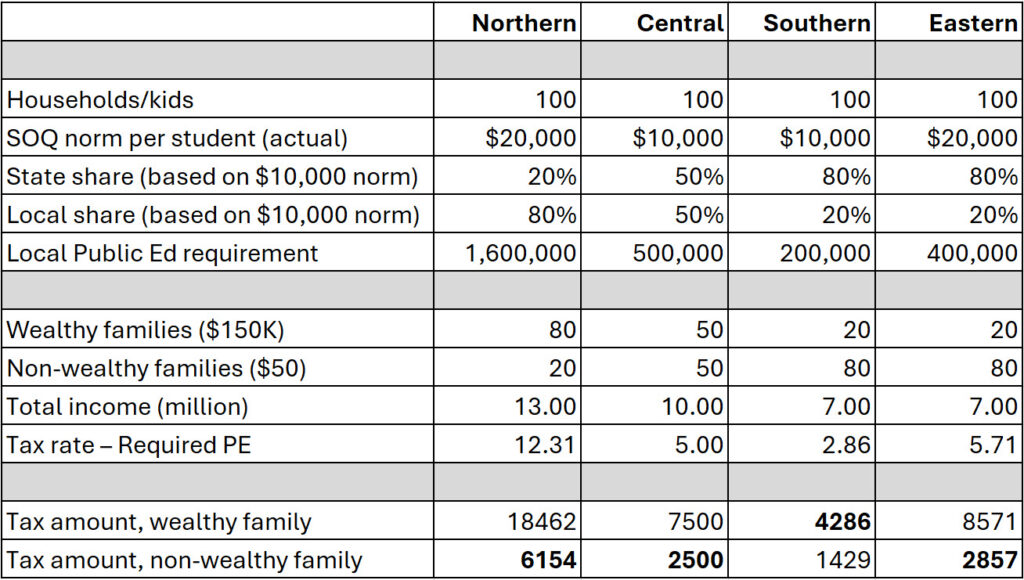

Let’s add one complicating factor: neither the cost of living, nor the cost of public education is constant in the four localities. Instead, urban localities (Northern and Eastern) tend to have higher costs, as well as higher demands for local public education spending. If the distribution of education grants does not take this into account—by simply funding the state’s relative share based on a cost norm of $10,000 per student in each of the four localities—the impact of the fiscal system becomes further skewed.

Numeric Example 2 (click toggle to view)

See Excel version (with formulas)

The numeric example shows that households in wealthier, higher-spending localities end up being taxed considerably more than households with the same income levels in less wealthy, lower-spending localities–even when comparing households with exactly the same incomes. In fact, in this scenario, low-income households in urban (higher-cost and/or wealthier) localities pay nearly as much (or pay more) to receive public education than high-income households in rural (lower-cost and/or poorer) localities.

So, the fiscal system is neither progressive or regressive based on income: instead, the fiscal system benefits taxpayers in certain places. The result is a system in which fiscal effort is not consistently rewarded, and in which the alignment between who pays and who benefits is weak.

The underlying political economy pattern

Virginia’s fiscal system does not reflect a coherent philosophy of public finance. It is not progressive, because it does not systematically redistribute resources based on ability to pay across the state. Nor does it reflect a clean model of limited government or low taxation, because it imposes substantial property tax obligations on some jurisdictions while allowing others to benefit from state-funded services without equivalent contributions.

Instead, the system produces a patchwork of outcomes shaped by geography, institutional arrangements, and historical compromises. The result is a form of redistribution that is untransparent and that runs counter to widely held notions of fairness.

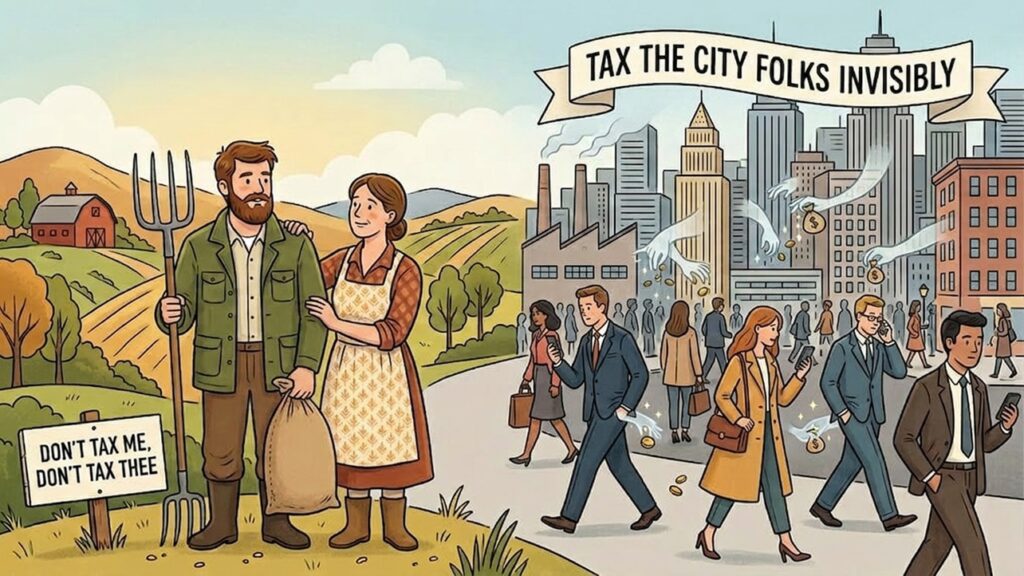

Specifically, the current system benefits taxpayers in some parts of the state (Southern and Central), at the expense of imposing a higher tax burden on other parts of the state (Northern and Eastern). Instead of the tax policy motto “Don’t tax me, don’t tax thee, tax the man behind the tree” attributed to former U.S. Senator Russell B. Long, Virginia seems to follow the alternative motto of “Don’t tax me, don’t tax thee, tax the city folks invisibly.”

These outcomes are not accidental; they reflect an underlying political economy reality that is common across many states and countries, based on a pattern that has dominated most political systems for centuries: rural voters tend to outnumber urban voters. (And in more recent decades, even if rural voters are not a majority, the political system may be structured to ensure that their political interests are overrepresented). If the majority of voters and politicians base their choices on their own self-interest rather than on their political convictions, than redistribution from wealthier urban places to less well-to-do rural places will occur (rather than from wealthy households to less wealthy households), even though a large swath of the electorate claims to be against redistribution. And as evidenced by the example above, both rich and poor taxpayers in the urban areas of the state will bear a disproportionate share of the state’s fiscal burden—even after considering differences in income levels. In the meantime, the state’s rural elites benefit from the prevailing fiscal redistribution.

Although not the topic of the current blog, it is not hard to see that such a political dynamic might be reinforced by certain prejudices. Petersburg, Norfolk, Manassas, and Fairfax County are among the localities with the highest local tax rates in Virginia, and perhaps not coincidentally, are among the most diverse cities and counties in the Commonwealth.

A better way to think about fairness

If Virginia were to reconsider its approach, a more coherent system would start by aligning revenue sources with the nature of the services being funded. Public education, which is inherently redistributive and central to equal opportunity, would be financed to a greater extent through broad-based, progressive state revenues. Local governments would retain meaningful autonomy, but within a framework that does not penalize jurisdictions that invest in public services or reward those that do not.

Until then, Virginia’s fiscal system will continue to answer the wrong question. Rather than asking who has the ability to pay, it implicitly asks where people happen to live. And that is a question that not only leads to the wrong kind of redistribution, but results in tensions within the commonwealth and reduces its economic competitiveness.